| | |  ดูแหล่งที่มาบน GitHub ดูแหล่งที่มาบน GitHub | |

Variational Inference (VI) ใช้การอนุมานแบบเบย์โดยประมาณว่าเป็นปัญหาการปรับให้เหมาะสมที่สุด และพยายามหาการกระจายแบบหลัง 'ตัวแทน' ที่ลดความแตกต่างของ KL กับส่วนหลังที่แท้จริง VI แบบไล่ระดับมักจะเร็วกว่าวิธี MCMC ซึ่งประกอบขึ้นเองตามธรรมชาติด้วยการปรับพารามิเตอร์แบบจำลองให้เหมาะสมที่สุด และให้ขอบเขตที่ต่ำกว่าในหลักฐานแบบจำลองที่สามารถนำมาใช้โดยตรงสำหรับการเปรียบเทียบแบบจำลอง การวินิจฉัยการลู่เข้า และการอนุมานที่ประกอบได้

ความน่าจะเป็นของ TensorFlow นำเสนอเครื่องมือสำหรับ VI ที่รวดเร็ว ยืดหยุ่น และปรับขนาดได้ซึ่งพอดีกับสแต็ก TFP อย่างเป็นธรรมชาติ เครื่องมือเหล่านี้ช่วยให้สามารถสร้างส่วนหลังของตัวแทนเสมือนที่มีโครงสร้างความแปรปรวนร่วมที่เกิดจากการแปลงเชิงเส้นหรือกระแสการทำให้เป็นมาตรฐาน

VI สามารถนำมาใช้ในการประมาณการคชกรรม ช่วงเวลาที่น่าเชื่อถือ สำหรับพารามิเตอร์ของรูปแบบการถดถอยที่จะประเมินผลกระทบของการรักษาต่างๆหรือคุณลักษณะสังเกตเกี่ยวกับผลของดอกเบี้ย ช่วงที่น่าเชื่อถือผูกมัดค่าของพารามิเตอร์ที่ไม่ได้สังเกตด้วยความน่าจะเป็นที่แน่นอน ตามการแจกแจงหลังของพารามิเตอร์ที่ปรับเงื่อนไขกับข้อมูลที่สังเกตได้ และให้สมมติฐานเกี่ยวกับการแจกแจงก่อนหน้าของพารามิเตอร์

ใน Colab นี้เราแสดงให้เห็นถึงวิธีการใช้ VI ที่จะได้รับช่วงเวลาที่น่าเชื่อถือสำหรับพารามิเตอร์ของคชกรรมเชิงเส้นแบบการถดถอยในระดับเรดอนวัดในบ้าน (โดยใช้ Gelman et al, ของ (2007) ชุดเรดอน. ดู ตัวอย่างที่คล้ายกัน ในสแตน) เราแสดงให้เห็นว่า TFP JointDistribution s รวมกับ bijectors ในการสร้างและพอดีกับสองประเภทของ posteriors ตัวแทนแสดงออก:

- การแจกแจงแบบปกติมาตรฐานที่แปลงโดยบล็อกเมทริกซ์ เมทริกซ์อาจสะท้อนถึงความเป็นอิสระในองค์ประกอบบางอย่างของส่วนหลังและการพึ่งพาอาศัยกัน เป็นการผ่อนคลายสมมติฐานของค่าความแปรปรวนร่วมหรือค่าความแปรปรวนร่วมแบบเต็ม

- ที่มีความซับซ้อนมากขึ้นความจุสูงกว่า ผกผันไหลอัต

หลังของตัวแทนเสมือนได้รับการฝึกฝนและเปรียบเทียบกับผลลัพธ์จากการตรวจวัดพื้นฐานด้านหลังตัวแทนเสมือนในสนาม เช่นเดียวกับตัวอย่างจากความจริงภาคพื้นดินจากแฮมิลตันเนียน มอนติคาร์โล

ภาพรวมของการอนุมานแบบแปรผันแบบเบย์

สมมติว่าเรามีขั้นตอนการกำเนิดต่อไปนี้ที่ \(\theta\) หมายถึงพารามิเตอร์สุ่ม \(\omega\) หมายถึงค่าพารามิเตอร์ที่กำหนดและ \(x_i\) มีคุณสมบัติและ \(y_i\) เป็นค่าเป้าหมายสำหรับการ \(i=1,\ldots,n\) สังเกตจุดข้อมูล: \ begin {ชิด } &\theta \sim r(\Theta) && \text{(Prior)}\ &\text{for } i = 1 \ldots n: \nonumber \ &\quad y_i \sim p(Y_i|x_i, \theta \ โอเมก้า) && \ ข้อความ {(โอกาส)} \ end {} ชิด

VI มีลักษณะดังนี้: $\newcommand{\E}{\operatorname{\mathbb{E} } } \newcommand{\K}{\operatorname{\mathbb{K} } } \newcommand{\defeq}{\overset {\tiny\text{def} }{=} } \DeclareMathOperator*{\argmin}{arg\,min}$

\ begin {จัด} - \ บันทึก P ({y_i} _i ^ n | {x_i} _i ^ n, \ omega) และ \ defeq - \ Log \ int \ textrm {d} \ theta \ r (\ theta) \ prod_i^np(y_i|x_i,\theta, \omega) && \text{(อินทิกรัลที่ยากมาก)} \ &= -\log \int \textrm{d}\theta\, q(\theta) \frac{1 }{q(\theta)} r(\theta) \prod_i^np(y_i|x_i,\theta, \omega) && \text{(คูณด้วย 1)}\ &\le - \int \textrm{d} \ theta \, Q (\ theta) \ Log \ frac {r (\ theta) \ prod_i ^ NP (y_i | x i, \ theta, \ omega)} {Q (\ theta)} && \ ข้อความ {(ความไม่เท่าเทียมกันของเซ่น )} \ & \ defeq \ E {Q (\ ที)} [- \ บันทึก P (y_i | x_i \ ที \ omega)] + \ K [Q (\ ที) R (\ ที)] \ & \ defeq \text{expected negative log likelihood"} + ปลาย \ ข้อความ {regularizer kl"} \ {} ชิด

(ในทางเทคนิคเราสมมติ \(q\) เป็น อย่างต่อเนื่อง เกี่ยวกับการ \(r\). ดูยัง ความไม่เท่าเทียมกันของเซ่น .)

เนื่องจากขอบเขตถือสำหรับ q ทั้งหมด จึงชัดเจนที่สุดสำหรับ:

\[q^*,w^* = \argmin_{q \in \mathcal{Q},\omega\in\mathbb{R}^d} \left\{ \sum_i^n\E_{q(\Theta)}\left[ -\log p(y_i|x_i,\Theta, \omega) \right] + \K[q(\Theta), r(\Theta)] \right\}\]

เกี่ยวกับคำศัพท์เราเรียกว่า

- \(q^*\) ว่า "หลังตัวแทน" และ

- \(\mathcal{Q}\) ว่า "ครอบครัวตัวแทน."

\(\omega^*\) หมายถึงค่าโอกาสสูงสุดของพารามิเตอร์ที่กำหนดเกี่ยวกับการสูญเสียที่หก ดู การสำรวจครั้งนี้ สำหรับข้อมูลเพิ่มเติมเกี่ยวกับการอนุมานแปรผัน

ตัวอย่าง: การถดถอยเชิงเส้นแบบลำดับชั้นแบบเบย์ในการวัดเรดอน

เรดอนเป็นก๊าซกัมมันตภาพรังสีที่เข้าสู่บ้านเรือนผ่านจุดสัมผัสพื้น เป็นสารก่อมะเร็งที่เป็นสาเหตุหลักของมะเร็งปอดในผู้ไม่สูบบุหรี่ ระดับเรดอนแตกต่างกันไปในแต่ละครัวเรือน

EPA ได้ทำการศึกษาระดับเรดอนในบ้าน 80,000 หลัง ตัวทำนายที่สำคัญสองประการคือ:

- ชั้นที่ใช้วัด (เรดอนสูงกว่าในห้องใต้ดิน)

- ระดับยูเรเนียมในเขต (ความสัมพันธ์เชิงบวกกับระดับเรดอน)

ทำนายระดับเรดอนในบ้านจัดกลุ่มตามเขตที่เป็นปัญหาคลาสสิกในการสร้างแบบจำลองคชกรรมลำดับชั้นนำโดย Gelman และฮิลล์ (2006) เราจะสร้างแบบจำลองเชิงเส้นแบบลำดับชั้นเพื่อทำนายการวัดเรดอนในบ้าน ซึ่งลำดับชั้นคือการจัดกลุ่มบ้านตามเขต เรามีความสนใจในช่วงเวลาที่น่าเชื่อถือสำหรับผลกระทบของสถานที่ (เคาน์ตี) ต่อระดับเรดอนของบ้านในมินนิโซตา เพื่อแยกผลกระทบนี้ แบบจำลองจะรวมผลกระทบของระดับพื้นและยูเรเนียมไว้ด้วย นอกจากนี้ เราจะรวมผลกระทบตามบริบทที่สอดคล้องกับพื้นเฉลี่ยที่ใช้การวัดโดยเคาน์ตี เพื่อที่ว่าหากมีความแตกต่างระหว่างเคาน์ตีของพื้นที่ซึ่งใช้การวัด ค่านี้ไม่ได้เกิดจากผลกระทบของเคาน์ตี

pip3 install -q tf-nightly tfp-nightly

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

import tensorflow as tf

import tensorflow_datasets as tfds

import tensorflow_probability as tfp

import warnings

tfd = tfp.distributions

tfb = tfp.bijectors

plt.rcParams['figure.facecolor'] = '1.'

# Load the Radon dataset from `tensorflow_datasets` and filter to data from

# Minnesota.

dataset = tfds.as_numpy(

tfds.load('radon', split='train').filter(

lambda x: x['features']['state'] == 'MN').batch(10**9))

# Dependent variable: Radon measurements by house.

dataset = next(iter(dataset))

radon_measurement = dataset['activity'].astype(np.float32)

radon_measurement[radon_measurement <= 0.] = 0.1

log_radon = np.log(radon_measurement)

# Measured uranium concentrations in surrounding soil.

uranium_measurement = dataset['features']['Uppm'].astype(np.float32)

log_uranium = np.log(uranium_measurement)

# County indicator.

county_strings = dataset['features']['county'].astype('U13')

unique_counties, county = np.unique(county_strings, return_inverse=True)

county = county.astype(np.int32)

num_counties = unique_counties.size

# Floor on which the measurement was taken.

floor_of_house = dataset['features']['floor'].astype(np.int32)

# Average floor by county (contextual effect).

county_mean_floor = []

for i in range(num_counties):

county_mean_floor.append(floor_of_house[county == i].mean())

county_mean_floor = np.array(county_mean_floor, dtype=log_radon.dtype)

floor_by_county = county_mean_floor[county]

แบบจำลองการถดถอยมีการระบุดังนี้:

\(\newcommand{\Normal}{\operatorname{\sf Normal} }\)\ begin {จัด} & \ ข้อความ {uranium_weight} \ ซิม \ ปกติ (0, 1) \ & \ ข้อความ {county_floor_weight} \ ซิม \ ปกติ (0, 1) \ & \ ข้อความ {สำหรับ} J = 1 \ ldots \text{num_counties}:\ &\quad \text{county_effect}_j \sim \Normal (0, \sigma_c)\ &\text{for } i = 1\ldots n:\ &\quad \mu_i = ( \ และ \ สี่เหลี่ยม \ สี่เหลี่ยม \ ข้อความ {อคติ} \ และ \ สี่เหลี่ยม \ สี่เหลี่ยม + \ ข้อความ {ผลเขต} {\ ข้อความ {เขต} _i} \ และ \ สี่เหลี่ยม \ สี่เหลี่ยม + \ ข้อความ {log_uranium} _i \ ข้อความครั้ง \ {uranium_weight } \ และ \ สี่เหลี่ยม \ สี่เหลี่ยม + \ ข้อความ {floor_of_house} _i \ times \ ข้อความ {floor_weight} \ และ \ สี่เหลี่ยม \ สี่เหลี่ยม + \ ข้อความ {floor_by เขต} {\ ข้อความ {เขต} _i} \ ข้อความครั้ง \ {county_floor_weight}) \ & \ สี่เหลี่ยม \ ข้อความ {log_radon} _i \ ซิม \ ปกติ (\ mu_i \ sigma_y) \ end {จัด} ซึ่ง \(i\) ดัชนีสังเกตและ \(\text{county}_i\) เป็นเขตที่ \(i\)สังเกต TH เป็น ถ่าย.

เราใช้เอฟเฟกต์สุ่มระดับเคาน์ตีเพื่อบันทึกความผันแปรทางภูมิศาสตร์ พารามิเตอร์ uranium_weight และ county_floor_weight ย่อม probabilistically และ floor_weight และคง bias มีกำหนด ตัวเลือกการสร้างแบบจำลองเหล่านี้มักเกิดขึ้นโดยพลการ และจัดทำขึ้นเพื่อจุดประสงค์ในการสาธิต VI บนแบบจำลองความน่าจะเป็นของความซับซ้อนที่เหมาะสม สำหรับการอภิปรายอย่างละเอียดมากขึ้นของการสร้างแบบจำลองหลายระดับที่มีผลกระทบคงที่และแบบสุ่มใน TFP โดยใช้ชุดข้อมูลเรดอนดู หลายแบบจำลองรองพื้น และ ฟิตติ้งเชิงเส้นทั่วไปผสมผลรุ่นใช้แปรผันอนุมาน

# Create variables for fixed effects.

floor_weight = tf.Variable(0.)

bias = tf.Variable(0.)

# Variables for scale parameters.

log_radon_scale = tfp.util.TransformedVariable(1., tfb.Exp())

county_effect_scale = tfp.util.TransformedVariable(1., tfb.Exp())

# Define the probabilistic graphical model as a JointDistribution.

@tfd.JointDistributionCoroutineAutoBatched

def model():

uranium_weight = yield tfd.Normal(0., scale=1., name='uranium_weight')

county_floor_weight = yield tfd.Normal(

0., scale=1., name='county_floor_weight')

county_effect = yield tfd.Sample(

tfd.Normal(0., scale=county_effect_scale),

sample_shape=[num_counties], name='county_effect')

yield tfd.Normal(

loc=(log_uranium * uranium_weight + floor_of_house* floor_weight

+ floor_by_county * county_floor_weight

+ tf.gather(county_effect, county, axis=-1)

+ bias),

scale=log_radon_scale[..., tf.newaxis],

name='log_radon')

# Pin the observed `log_radon` values to model the un-normalized posterior.

target_model = model.experimental_pin(log_radon=log_radon)

หลังตัวแทนแสดงออกชัดเจน

ต่อไป เราประมาณการการแจกแจงภายหลังของเอฟเฟกต์สุ่มโดยใช้ VI กับตัวแทนหลังสองประเภทที่แตกต่างกัน:

- การแจกแจงแบบปกติหลายตัวแปรที่มีข้อจำกัด โดยมีโครงสร้างความแปรปรวนร่วมที่เกิดจากการแปลงเมทริกซ์แบบบล็อก

- หลายตัวแปรกระจายมาตรฐานปกติเปลี่ยนโดย ผกผันอัตถดถอยไหล ซึ่งถูกแบ่งออกแล้วและการปรับโครงสร้างหนี้เพื่อให้ตรงกับการสนับสนุนของหลังที่

หลายตัวแปร ปกติ ตัวแทนหลัง

ในการสร้างตัวแทนส่วนหลังนี้ ตัวดำเนินการเชิงเส้นที่ฝึกได้จะถูกนำมาใช้เพื่อสร้างความสัมพันธ์ระหว่างส่วนประกอบต่างๆ ของส่วนหลัง

# Determine the `event_shape` of the posterior, and calculate the size of each

# `event_shape` component. These determine the sizes of the components of the

# underlying standard Normal distribution, and the dimensions of the blocks in

# the blockwise matrix transformation.

event_shape = target_model.event_shape_tensor()

flat_event_shape = tf.nest.flatten(event_shape)

flat_event_size = tf.nest.map_structure(tf.reduce_prod, flat_event_shape)

# The `event_space_bijector` maps unconstrained values (in R^n) to the support

# of the prior -- we'll need this at the end to constrain Multivariate Normal

# samples to the prior's support.

event_space_bijector = target_model.experimental_default_event_space_bijector()

สร้าง JointDistribution มีส่วนประกอบปกติเวกเตอร์มาตรฐานที่มีขนาดที่กำหนดโดยส่วนประกอบก่อนที่สอดคล้องกัน ส่วนประกอบควรมีค่าเวกเตอร์เพื่อให้สามารถเปลี่ยนแปลงได้โดยตัวดำเนินการเชิงเส้น

base_standard_dist = tfd.JointDistributionSequential(

[tfd.Sample(tfd.Normal(0., 1.), s) for s in flat_event_size])

สร้างตัวดำเนินการเชิงเส้นตรงรูปสามเหลี่ยมล่างแบบบล็อกขวางที่ฝึกได้ เราจะนำไปใช้กับการแจกแจงแบบปกติมาตรฐานเพื่อใช้การแปลงเมทริกซ์แบบบล็อก (ฝึกได้) และกระตุ้นโครงสร้างความสัมพันธ์ของส่วนหลัง

ภายใน blockwise เชิงเส้นผู้ประกอบการที่เป็นสุวินัยบล็อกเต็มรูปแบบเมทริกซ์แสดงให้เห็นถึงความแปรปรวนเต็มระหว่างสองส่วนหลังในขณะที่บล็อกของศูนย์ (หรือ None ) เป็นการแสดงออกถึงความเป็นอิสระ บล็อกในแนวทแยงเป็นเมทริกซ์รูปสามเหลี่ยมล่างหรือแนวทแยง เพื่อให้โครงสร้างบล็อกทั้งหมดแสดงเมทริกซ์สามเหลี่ยมล่าง

การใช้ bijector นี้กับการกระจายฐานส่งผลให้เกิดการแจกแจงแบบปกติหลายตัวแปรที่มีค่าความแปรปรวนร่วมเฉลี่ย 0 และ (Cholesky-factored) เท่ากับเมทริกซ์บล็อกสามเหลี่ยมล่าง

operators = (

(tf.linalg.LinearOperatorDiag,), # Variance of uranium weight (scalar).

(tf.linalg.LinearOperatorFullMatrix, # Covariance between uranium and floor-by-county weights.

tf.linalg.LinearOperatorDiag), # Variance of floor-by-county weight (scalar).

(None, # Independence between uranium weight and county effects.

None, # Independence between floor-by-county and county effects.

tf.linalg.LinearOperatorDiag) # Independence among the 85 county effects.

)

block_tril_linop = (

tfp.experimental.vi.util.build_trainable_linear_operator_block(

operators, flat_event_size))

scale_bijector = tfb.ScaleMatvecLinearOperatorBlock(block_tril_linop)

หลังจากใช้ผู้ประกอบการเชิงเส้นการกระจายปกติมาตรฐานใช้ multipart Shift bijector เพื่อให้ค่าเฉลี่ยจะใช้ค่าเป็นศูนย์

loc_bijector = tfb.JointMap(

tf.nest.map_structure(

lambda s: tfb.Shift(

tf.Variable(tf.random.uniform(

(s,), minval=-2., maxval=2., dtype=tf.float32))),

flat_event_size))

ผลการแจกแจงแบบ Normal หลายตัวแปรที่ได้มาจากการเปลี่ยนรูปแบบการแจกแจง Normal มาตรฐานด้วยตัวปรับขนาดและตำแหน่ง bijectors จะต้องถูกปรับโฉมและจัดโครงสร้างใหม่เพื่อให้ตรงกับค่าก่อนหน้า และสุดท้ายถูกจำกัดให้รองรับค่าก่อนหน้า

# Reshape each component to match the prior, using a nested structure of

# `Reshape` bijectors wrapped in `JointMap` to form a multipart bijector.

reshape_bijector = tfb.JointMap(

tf.nest.map_structure(tfb.Reshape, flat_event_shape))

# Restructure the flat list of components to match the prior's structure

unflatten_bijector = tfb.Restructure(

tf.nest.pack_sequence_as(

event_shape, range(len(flat_event_shape))))

ตอนนี้ นำมันมารวมกัน -- โยง bijectors ที่ฝึกได้เข้าด้วยกันและนำไปใช้กับมาตรฐานฐาน การแจกแจงแบบปกติเพื่อสร้างส่วนหลังตัวแทน

surrogate_posterior = tfd.TransformedDistribution(

base_standard_dist,

bijector = tfb.Chain( # Note that the chained bijectors are applied in reverse order

[

event_space_bijector, # constrain the surrogate to the support of the prior

unflatten_bijector, # pack the reshaped components into the `event_shape` structure of the posterior

reshape_bijector, # reshape the vector-valued components to match the shapes of the posterior components

loc_bijector, # allow for nonzero mean

scale_bijector # apply the block matrix transformation to the standard Normal distribution

]))

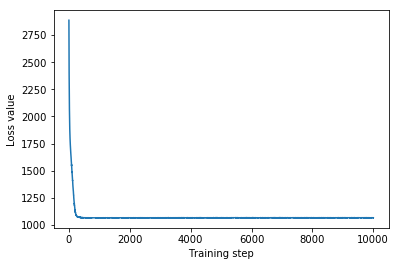

ฝึกตัวแทนพหุตัวแปรหลังปกติ

optimizer = tf.optimizers.Adam(learning_rate=1e-2)

mvn_loss = tfp.vi.fit_surrogate_posterior(

target_model.unnormalized_log_prob,

surrogate_posterior,

optimizer=optimizer,

num_steps=10**4,

sample_size=16,

jit_compile=True)

mvn_samples = surrogate_posterior.sample(1000)

mvn_final_elbo = tf.reduce_mean(

target_model.unnormalized_log_prob(*mvn_samples)

- surrogate_posterior.log_prob(mvn_samples))

print('Multivariate Normal surrogate posterior ELBO: {}'.format(mvn_final_elbo))

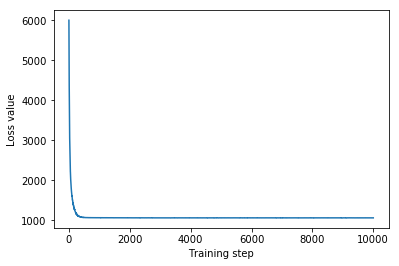

plt.plot(mvn_loss)

plt.xlabel('Training step')

_ = plt.ylabel('Loss value')

Multivariate Normal surrogate posterior ELBO: -1065.705322265625

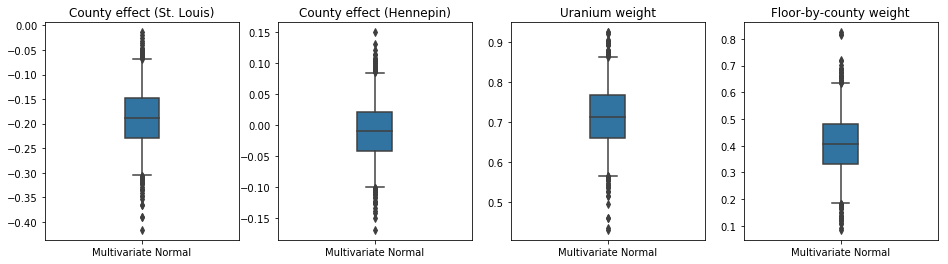

เนื่องจากตัวแทนหลังที่ผ่านการฝึกอบรมเป็นการแจกแจง TFP เราจึงสามารถนำตัวอย่างจากตัวอย่างนั้นและประมวลผลเพื่อสร้างช่วงหลังที่น่าเชื่อถือสำหรับพารามิเตอร์

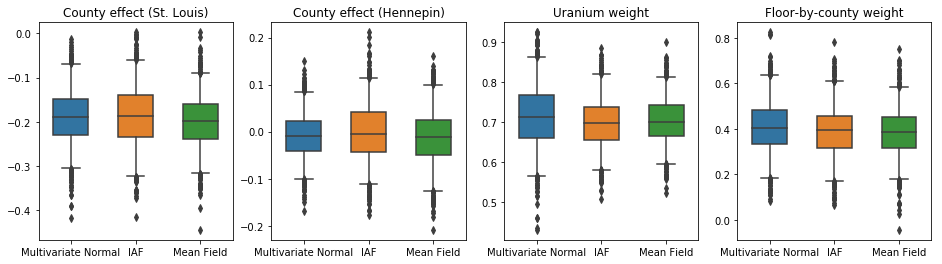

กล่องและเคราแปลงด้านล่างจะแสดง 50% และ 95% ช่วงเวลาที่น่าเชื่อถือ สำหรับผลเขตของสองมณฑลที่ใหญ่ที่สุดและน้ำหนักถดถอยวัดยูเรเนียมดินและพื้นเฉลี่ยโดยมณฑล ช่วงหลังที่น่าเชื่อถือสำหรับผลกระทบของเคาน์ตีบ่งชี้ว่าที่ตั้งในเขตเซนต์หลุยส์มีความเกี่ยวข้องกับระดับเรดอนที่ต่ำกว่า หลังจากพิจารณาตัวแปรอื่นๆ และผลกระทบของตำแหน่งในเคาน์ตีเฮนเนพินนั้นใกล้จะเป็นกลาง

ช่วงหลังที่น่าเชื่อถือของตุ้มน้ำหนักการถดถอยแสดงให้เห็นว่าระดับยูเรเนียมในดินที่สูงขึ้นมีความสัมพันธ์กับระดับเรดอนที่สูงขึ้น และเขตที่มีการตรวจวัดบนชั้นที่สูงขึ้น (อาจเป็นเพราะบ้านไม่มีชั้นใต้ดิน) มักจะมีระดับเรดอนสูงกว่า ซึ่งอาจเกี่ยวข้องกับคุณสมบัติของดินและผลกระทบต่อประเภทของโครงสร้างที่สร้างขึ้น

ค่าสัมประสิทธิ์ของพื้น (ที่กำหนดขึ้นเอง) เป็นค่าลบ ซึ่งบ่งชี้ว่าชั้นล่างมีระดับเรดอนสูงกว่าที่คาดไว้

st_louis_co = 69 # Index of St. Louis, the county with the most observations.

hennepin_co = 25 # Index of Hennepin, with the second-most observations.

def pack_samples(samples):

return {'County effect (St. Louis)': samples.county_effect[..., st_louis_co],

'County effect (Hennepin)': samples.county_effect[..., hennepin_co],

'Uranium weight': samples.uranium_weight,

'Floor-by-county weight': samples.county_floor_weight}

def plot_boxplot(posterior_samples):

fig, axes = plt.subplots(1, 4, figsize=(16, 4))

# Invert the results dict for easier plotting.

k = list(posterior_samples.values())[0].keys()

plot_results = {

v: {p: posterior_samples[p][v] for p in posterior_samples} for v in k}

for i, (var, var_results) in enumerate(plot_results.items()):

sns.boxplot(data=list(var_results.values()), ax=axes[i],

width=0.18*len(var_results), whis=(2.5, 97.5))

# axes[i].boxplot(list(var_results.values()), whis=(2.5, 97.5))

axes[i].title.set_text(var)

fs = 10 if len(var_results) < 4 else 8

axes[i].set_xticklabels(list(var_results.keys()), fontsize=fs)

results = {'Multivariate Normal': pack_samples(mvn_samples)}

print('Bias is: {:.2f}'.format(bias.numpy()))

print('Floor fixed effect is: {:.2f}'.format(floor_weight.numpy()))

plot_boxplot(results)

Bias is: 1.40 Floor fixed effect is: -0.72

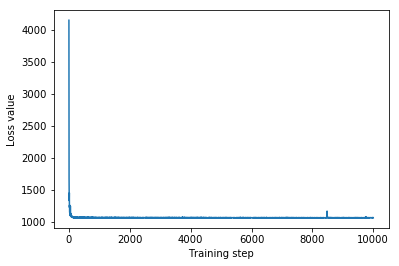

Inverse Autoregressive Flow ตัวแทนหลัง

Inverse Autoregressive Flows (IAFs) เป็นกระแสที่ทำให้เป็นมาตรฐานซึ่งใช้โครงข่ายประสาทเทียมเพื่อจับภาพการพึ่งพาที่ซับซ้อนและไม่เชิงเส้นระหว่างส่วนประกอบของการกระจาย ต่อไป เราสร้างตัวแทนเสมือนด้านหลังเพื่อดูว่าโมเดลที่มีความจุสูงกว่าและปรับเปลี่ยนได้ดีกว่านี้มีประสิทธิภาพเหนือกว่าตัวแปรหลายตัวแปรที่มีข้อจำกัด Normal หรือไม่

# Build a standard Normal with a vector `event_shape`, with length equal to the

# total number of degrees of freedom in the posterior.

base_distribution = tfd.Sample(

tfd.Normal(0., 1.), sample_shape=[tf.reduce_sum(flat_event_size)])

# Apply an IAF to the base distribution.

num_iafs = 2

iaf_bijectors = [

tfb.Invert(tfb.MaskedAutoregressiveFlow(

shift_and_log_scale_fn=tfb.AutoregressiveNetwork(

params=2, hidden_units=[256, 256], activation='relu')))

for _ in range(num_iafs)

]

# Split the base distribution's `event_shape` into components that are equal

# in size to the prior's components.

split = tfb.Split(flat_event_size)

# Chain these bijectors and apply them to the standard Normal base distribution

# to build the surrogate posterior. `event_space_bijector`,

# `unflatten_bijector`, and `reshape_bijector` are the same as in the

# multivariate Normal surrogate posterior.

iaf_surrogate_posterior = tfd.TransformedDistribution(

base_distribution,

bijector=tfb.Chain([

event_space_bijector, # constrain the surrogate to the support of the prior

unflatten_bijector, # pack the reshaped components into the `event_shape` structure of the prior

reshape_bijector, # reshape the vector-valued components to match the shapes of the prior components

split] + # Split the samples into components of the same size as the prior components

iaf_bijectors # Apply a flow model to the Tensor-valued standard Normal distribution

))

ฝึกตัวแทน IAF หลัง

optimizer=tf.optimizers.Adam(learning_rate=1e-2)

iaf_loss = tfp.vi.fit_surrogate_posterior(

target_model.unnormalized_log_prob,

iaf_surrogate_posterior,

optimizer=optimizer,

num_steps=10**4,

sample_size=4,

jit_compile=True)

iaf_samples = iaf_surrogate_posterior.sample(1000)

iaf_final_elbo = tf.reduce_mean(

target_model.unnormalized_log_prob(*iaf_samples)

- iaf_surrogate_posterior.log_prob(iaf_samples))

print('IAF surrogate posterior ELBO: {}'.format(iaf_final_elbo))

plt.plot(iaf_loss)

plt.xlabel('Training step')

_ = plt.ylabel('Loss value')

IAF surrogate posterior ELBO: -1065.3663330078125

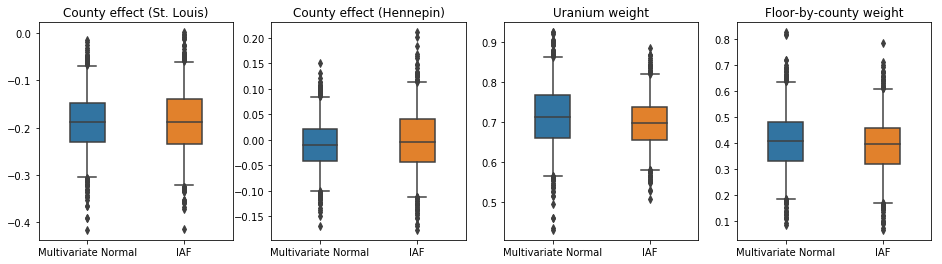

ช่วงที่น่าเชื่อถือสำหรับหลังตัวแทน IAF นั้นคล้ายคลึงกับช่วงปกติที่มีหลายตัวแปรที่มีข้อจำกัด

results['IAF'] = pack_samples(iaf_samples)

plot_boxplot(results)

พื้นฐาน: หลังตัวแทนเสมือนสนามกลาง

VI ตัวแทนหลังมักจะถูกสันนิษฐานว่าเป็นค่าเฉลี่ยฟิลด์ (อิสระ) การแจกแจงแบบปกติด้วยค่าเฉลี่ยและความแปรปรวนที่ฝึกได้ซึ่งถูก จำกัด ให้สนับสนุนก่อนหน้านี้ด้วยการเปลี่ยนแปลงแบบสองทาง เรากำหนดส่วนหลังของตัวแทนเสมือนที่มีฟิลด์กลางเพิ่มเติมจากส่วนหลังของตัวแทนเสมือนที่แสดงอารมณ์อีกสองคน โดยใช้สูตรทั่วไปเดียวกันกับส่วนหลังของตัวแทนเสมือนหลายตัวแปร

# A block-diagonal linear operator, in which each block is a diagonal operator,

# transforms the standard Normal base distribution to produce a mean-field

# surrogate posterior.

operators = (tf.linalg.LinearOperatorDiag,

tf.linalg.LinearOperatorDiag,

tf.linalg.LinearOperatorDiag)

block_diag_linop = (

tfp.experimental.vi.util.build_trainable_linear_operator_block(

operators, flat_event_size))

mean_field_scale = tfb.ScaleMatvecLinearOperatorBlock(block_diag_linop)

mean_field_loc = tfb.JointMap(

tf.nest.map_structure(

lambda s: tfb.Shift(

tf.Variable(tf.random.uniform(

(s,), minval=-2., maxval=2., dtype=tf.float32))),

flat_event_size))

mean_field_surrogate_posterior = tfd.TransformedDistribution(

base_standard_dist,

bijector = tfb.Chain( # Note that the chained bijectors are applied in reverse order

[

event_space_bijector, # constrain the surrogate to the support of the prior

unflatten_bijector, # pack the reshaped components into the `event_shape` structure of the posterior

reshape_bijector, # reshape the vector-valued components to match the shapes of the posterior components

mean_field_loc, # allow for nonzero mean

mean_field_scale # apply the block matrix transformation to the standard Normal distribution

]))

optimizer=tf.optimizers.Adam(learning_rate=1e-2)

mean_field_loss = tfp.vi.fit_surrogate_posterior(

target_model.unnormalized_log_prob,

mean_field_surrogate_posterior,

optimizer=optimizer,

num_steps=10**4,

sample_size=16,

jit_compile=True)

mean_field_samples = mean_field_surrogate_posterior.sample(1000)

mean_field_final_elbo = tf.reduce_mean(

target_model.unnormalized_log_prob(*mean_field_samples)

- mean_field_surrogate_posterior.log_prob(mean_field_samples))

print('Mean-field surrogate posterior ELBO: {}'.format(mean_field_final_elbo))

plt.plot(mean_field_loss)

plt.xlabel('Training step')

_ = plt.ylabel('Loss value')

Mean-field surrogate posterior ELBO: -1065.7652587890625

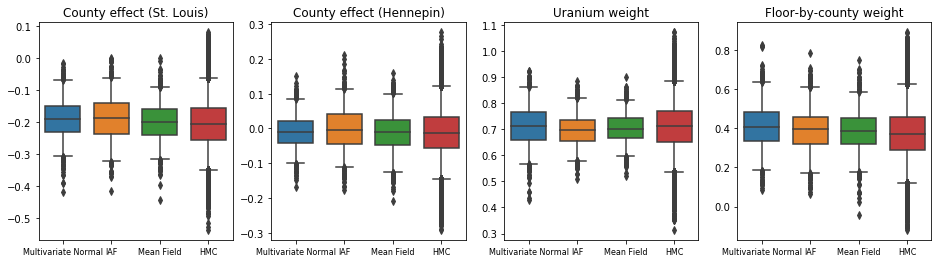

ในกรณีนี้ ค่าเฉลี่ยหลังตัวแทนภาคสนามจะให้ผลลัพธ์ที่คล้ายคลึงกันกับกลุ่มหลังตัวแทนที่แสดงออกมากขึ้น ซึ่งบ่งชี้ว่าแบบจำลองที่เรียบง่ายกว่านี้อาจเพียงพอสำหรับงานอนุมาน

results['Mean Field'] = pack_samples(mean_field_samples)

plot_boxplot(results)

ความจริงพื้นฐาน: Hamiltonian Monte Carlo (HMC)

เราใช้ HMC เพื่อสร้างตัวอย่าง "ความจริงพื้นฐาน" จากส่วนหลังที่แท้จริง เพื่อเปรียบเทียบกับผลลัพธ์ของตัวแทนส่วนหลัง

num_chains = 8

num_leapfrog_steps = 3

step_size = 0.4

num_steps=20000

flat_event_shape = tf.nest.flatten(target_model.event_shape)

enum_components = list(range(len(flat_event_shape)))

bijector = tfb.Restructure(

enum_components,

tf.nest.pack_sequence_as(target_model.event_shape, enum_components))(

target_model.experimental_default_event_space_bijector())

current_state = bijector(

tf.nest.map_structure(

lambda e: tf.zeros([num_chains] + list(e), dtype=tf.float32),

target_model.event_shape))

hmc = tfp.mcmc.HamiltonianMonteCarlo(

target_log_prob_fn=target_model.unnormalized_log_prob,

num_leapfrog_steps=num_leapfrog_steps,

step_size=[tf.fill(s.shape, step_size) for s in current_state])

hmc = tfp.mcmc.TransformedTransitionKernel(

hmc, bijector)

hmc = tfp.mcmc.DualAveragingStepSizeAdaptation(

hmc,

num_adaptation_steps=int(num_steps // 2 * 0.8),

target_accept_prob=0.9)

chain, is_accepted = tf.function(

lambda current_state: tfp.mcmc.sample_chain(

current_state=current_state,

kernel=hmc,

num_results=num_steps // 2,

num_burnin_steps=num_steps // 2,

trace_fn=lambda _, pkr:

(pkr.inner_results.inner_results.is_accepted),

),

autograph=False,

jit_compile=True)(current_state)

accept_rate = tf.reduce_mean(tf.cast(is_accepted, tf.float32))

ess = tf.nest.map_structure(

lambda c: tfp.mcmc.effective_sample_size(

c,

cross_chain_dims=1,

filter_beyond_positive_pairs=True),

chain)

r_hat = tf.nest.map_structure(tfp.mcmc.potential_scale_reduction, chain)

hmc_samples = pack_samples(

tf.nest.pack_sequence_as(target_model.event_shape, chain))

print('Acceptance rate is {}'.format(accept_rate))

Acceptance rate is 0.9008625149726868

พล็อตการติดตามตัวอย่างไปยังผลลัพธ์ HMC ของการตรวจสุขภาพจิต

def plot_traces(var_name, samples):

fig, axes = plt.subplots(1, 2, figsize=(14, 1.5), sharex='col', sharey='col')

for chain in range(num_chains):

s = samples.numpy()[:, chain]

axes[0].plot(s, alpha=0.7)

sns.kdeplot(s, ax=axes[1], shade=False)

axes[0].title.set_text("'{}' trace".format(var_name))

axes[1].title.set_text("'{}' distribution".format(var_name))

axes[0].set_xlabel('Iteration')

warnings.filterwarnings('ignore')

for var, var_samples in hmc_samples.items():

plot_traces(var, var_samples)

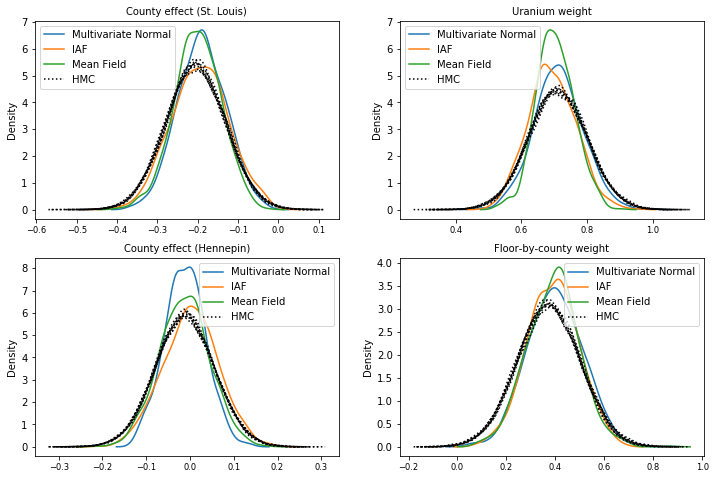

ตัวแทนหลังทั้งสามสร้างช่วงเวลาที่น่าเชื่อถือซึ่งมองเห็นได้คล้ายกับตัวอย่าง HMC แม้ว่าบางครั้งอาจกระจายไม่ทั่วถึงเนื่องจากผลกระทบของการสูญเสีย ELBO ตามปกติใน VI

results['HMC'] = hmc_samples

plot_boxplot(results)

ผลลัพธ์เพิ่มเติม

ฟังก์ชันพล็อต

plt.rcParams.update({'axes.titlesize': 'medium', 'xtick.labelsize': 'medium'})

def plot_loss_and_elbo():

fig, axes = plt.subplots(1, 2, figsize=(12, 4))

axes[0].scatter([0, 1, 2],

[mvn_final_elbo.numpy(),

iaf_final_elbo.numpy(),

mean_field_final_elbo.numpy()])

axes[0].set_xticks(ticks=[0, 1, 2])

axes[0].set_xticklabels(labels=[

'Multivariate Normal', 'IAF', 'Mean Field'])

axes[0].title.set_text('Evidence Lower Bound (ELBO)')

axes[1].plot(mvn_loss, label='Multivariate Normal')

axes[1].plot(iaf_loss, label='IAF')

axes[1].plot(mean_field_loss, label='Mean Field')

axes[1].set_ylim([1000, 4000])

axes[1].set_xlabel('Training step')

axes[1].set_ylabel('Loss (negative ELBO)')

axes[1].title.set_text('Loss')

plt.legend()

plt.show()

plt.rcParams.update({'axes.titlesize': 'medium', 'xtick.labelsize': 'small'})

def plot_kdes(num_chains=8):

fig, axes = plt.subplots(2, 2, figsize=(12, 8))

k = list(results.values())[0].keys()

plot_results = {

v: {p: results[p][v] for p in results} for v in k}

for i, (var, var_results) in enumerate(plot_results.items()):

ax = axes[i % 2, i // 2]

for posterior, posterior_results in var_results.items():

if posterior == 'HMC':

label = posterior

for chain in range(num_chains):

sns.kdeplot(

posterior_results[:, chain],

ax=ax, shade=False, color='k', linestyle=':', label=label)

label=None

else:

sns.kdeplot(

posterior_results, ax=ax, shade=False, label=posterior)

ax.title.set_text('{}'.format(var))

ax.legend()

หลักฐานขอบเขตล่าง (ELBO)

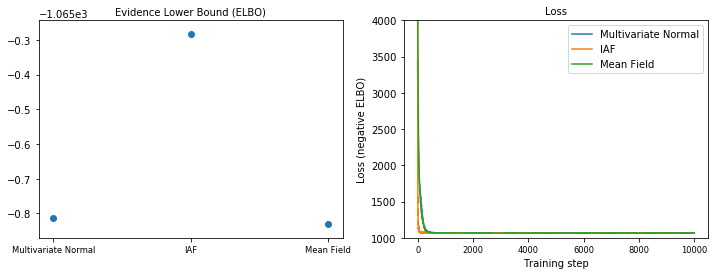

IAF ซึ่งเป็นกลุ่มหลังตัวแทนที่ใหญ่ที่สุดและยืดหยุ่นที่สุด มาบรรจบกันที่ขอบเขตล่างสุดของหลักฐาน (ELBO)

plot_loss_and_elbo()

ตัวอย่างหลัง

ตัวอย่างจากตัวแทนหลังแต่ละคน เปรียบเทียบกับตัวอย่างความจริงภาคพื้นดินของ HMC (การแสดงภาพตัวอย่างที่แสดงในแผนภาพกล่องที่ต่างกัน)

plot_kdes()

บทสรุป

ใน Colab นี้ เราสร้าง VI ตัวแทนหลังโดยใช้การแจกแจงร่วมและ bijectors แบบหลายส่วน และปรับให้เหมาะสมเพื่อประมาณช่วงเวลาที่น่าเชื่อถือสำหรับน้ำหนักในแบบจำลองการถดถอยบนชุดข้อมูลเรดอน สำหรับโมเดลที่เรียบง่ายนี้ ตัวแทนหลังที่แสดงอารมณ์ได้ชัดเจนกว่าจะแสดงในลักษณะเดียวกับหลังตัวแทนตัวแทนที่มีใจกว้าง อย่างไรก็ตาม เครื่องมือที่เราสาธิตสามารถใช้เพื่อสร้างส่วนหลังของตัวแทนเสมือนที่ยืดหยุ่นได้หลากหลาย ซึ่งเหมาะสำหรับโมเดลที่ซับซ้อนมากขึ้น