| | |  ดูแหล่งที่มาบน GitHub ดูแหล่งที่มาบน GitHub | |

ความน่าจะเป็นการวิเคราะห์องค์ประกอบหลัก (PCA) เป็นเทคนิคการลดมิติที่ช่วยวิเคราะห์ข้อมูลผ่านพื้นที่แฝงมิติที่ต่ำกว่า ( Tipping และบิชอป 1999 ) มักใช้เมื่อมีค่าที่ขาดหายไปในข้อมูลหรือสำหรับการปรับขนาดหลายมิติ

นำเข้า

import functools

import warnings

import matplotlib.pyplot as plt

import numpy as np

import seaborn as sns

import tensorflow.compat.v2 as tf

import tensorflow_probability as tfp

from tensorflow_probability import bijectors as tfb

from tensorflow_probability import distributions as tfd

tf.enable_v2_behavior()

plt.style.use("ggplot")

warnings.filterwarnings('ignore')

นางแบบ

พิจารณาข้อมูลชุด \(\mathbf{X} = \{\mathbf{x}_n\}\) ของ \(N\) จุดข้อมูลที่แต่ละจุดข้อมูลเป็น \(D\)มิติ, $ \ mathbf {x} _n \ in \ mathbb {R} ^ D\(. We aim to represent each \)\ mathbf {x} _n ภายใต้ $ ตัวแปรแฝง \(\mathbf{z}_n \in \mathbb{R}^K\) กับมิติที่ต่ำกว่า $ K <D\(. The set of principal axes \)\ mathbf {W} $ เกี่ยวข้องตัวแปรแฝงข้อมูล

โดยเฉพาะอย่างยิ่ง เราคิดว่าตัวแปรแฝงแต่ละตัวมีการกระจายตามปกติ

\[ \begin{equation*} \mathbf{z}_n \sim N(\mathbf{0}, \mathbf{I}). \end{equation*} \]

จุดข้อมูลที่สอดคล้องกันถูกสร้างขึ้นผ่านการฉายภาพ

\[ \begin{equation*} \mathbf{x}_n \mid \mathbf{z}_n \sim N(\mathbf{W}\mathbf{z}_n, \sigma^2\mathbf{I}), \end{equation*} \]

ที่เมทริกซ์ \(\mathbf{W}\in\mathbb{R}^{D\times K}\) เป็นที่รู้จักกันเป็นแกนหลัก ใน PCA น่าจะเป็นเรามักจะมีความสนใจในการประมาณแกนหลัก \(\mathbf{W}\) และระยะเสียง\(\sigma^2\)

PCA ความน่าจะเป็นโดยทั่วไป PCA แบบคลาสสิก การหาระยะขอบของตัวแปรแฝง การกระจายของจุดข้อมูลแต่ละจุดคือ

\[ \begin{equation*} \mathbf{x}_n \sim N(\mathbf{0}, \mathbf{W}\mathbf{W}^\top + \sigma^2\mathbf{I}). \end{equation*} \]

PCA คลาสสิกเป็นกรณีที่เฉพาะเจาะจงของ PCA น่าจะเป็นเมื่อความแปรปรวนของเสียงจะกลายเป็นขนาดเล็กกระจิริด \(\sigma^2 \to 0\)

เราตั้งค่าโมเดลของเราด้านล่าง ในการวิเคราะห์ของเราเราถือว่า \(\sigma\) เป็นที่รู้จักกันและแทนการจุดประมาณ \(\mathbf{W}\) เป็นพารามิเตอร์รุ่นเราวางก่อนที่มากกว่านั้นเพื่อที่จะสรุปการจัดจำหน่ายมากกว่าแกนหลัก เราจะแสดงรูปแบบเป็น TFP JointDistribution เฉพาะเราจะใช้ JointDistributionCoroutineAutoBatched

def probabilistic_pca(data_dim, latent_dim, num_datapoints, stddv_datapoints):

w = yield tfd.Normal(loc=tf.zeros([data_dim, latent_dim]),

scale=2.0 * tf.ones([data_dim, latent_dim]),

name="w")

z = yield tfd.Normal(loc=tf.zeros([latent_dim, num_datapoints]),

scale=tf.ones([latent_dim, num_datapoints]),

name="z")

x = yield tfd.Normal(loc=tf.matmul(w, z),

scale=stddv_datapoints,

name="x")

num_datapoints = 5000

data_dim = 2

latent_dim = 1

stddv_datapoints = 0.5

concrete_ppca_model = functools.partial(probabilistic_pca,

data_dim=data_dim,

latent_dim=latent_dim,

num_datapoints=num_datapoints,

stddv_datapoints=stddv_datapoints)

model = tfd.JointDistributionCoroutineAutoBatched(concrete_ppca_model)

ข้อมูล

เราสามารถใช้แบบจำลองเพื่อสร้างข้อมูลโดยการสุ่มตัวอย่างจากการแจกแจงร่วมกันก่อน

actual_w, actual_z, x_train = model.sample()

print("Principal axes:")

print(actual_w)

Principal axes: tf.Tensor( [[ 2.2801023] [-1.1619819]], shape=(2, 1), dtype=float32)

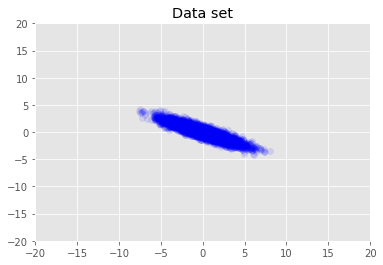

เราเห็นภาพชุดข้อมูล

plt.scatter(x_train[0, :], x_train[1, :], color='blue', alpha=0.1)

plt.axis([-20, 20, -20, 20])

plt.title("Data set")

plt.show()

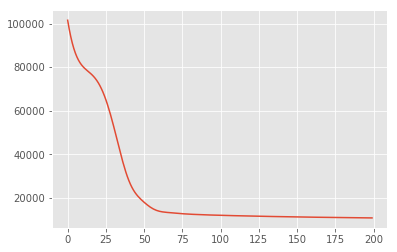

การอนุมาน Posteriori สูงสุด

ก่อนอื่นเราค้นหาการประมาณค่าจุดของตัวแปรแฝงที่เพิ่มความหนาแน่นของความน่าจะเป็นภายหลังสูงสุด นี้เป็นที่รู้จักกันเป็นสูงสุด posteriori (MAP) การอนุมานและจะทำโดยการคำนวณค่าของ \(\mathbf{W}\) และ \(\mathbf{Z}\) ที่เพิ่มความหนาแน่นหลัง \(p(\mathbf{W}, \mathbf{Z} \mid \mathbf{X}) \propto p(\mathbf{W}, \mathbf{Z}, \mathbf{X})\)

w = tf.Variable(tf.random.normal([data_dim, latent_dim]))

z = tf.Variable(tf.random.normal([latent_dim, num_datapoints]))

target_log_prob_fn = lambda w, z: model.log_prob((w, z, x_train))

losses = tfp.math.minimize(

lambda: -target_log_prob_fn(w, z),

optimizer=tf.optimizers.Adam(learning_rate=0.05),

num_steps=200)

plt.plot(losses)

[<matplotlib.lines.Line2D at 0x7f19897a42e8>]

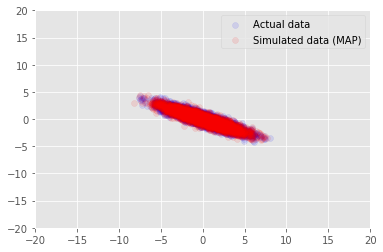

เราสามารถใช้แบบจำลองเพื่อใช้ข้อมูลตัวอย่างสำหรับค่าอนุมานสำหรับ \(\mathbf{W}\) และ \(\mathbf{Z}\)และเปรียบเทียบกับชุดข้อมูลที่เกิดขึ้นจริงเราปรับอากาศบน

print("MAP-estimated axes:")

print(w)

_, _, x_generated = model.sample(value=(w, z, None))

plt.scatter(x_train[0, :], x_train[1, :], color='blue', alpha=0.1, label='Actual data')

plt.scatter(x_generated[0, :], x_generated[1, :], color='red', alpha=0.1, label='Simulated data (MAP)')

plt.legend()

plt.axis([-20, 20, -20, 20])

plt.show()

MAP-estimated axes:

<tf.Variable 'Variable:0' shape=(2, 1) dtype=float32, numpy=

array([[ 2.9135954],

[-1.4826864]], dtype=float32)>

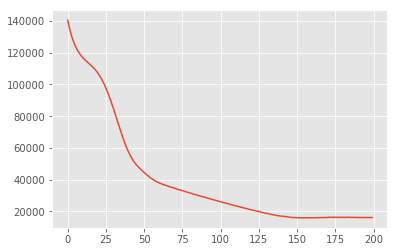

การอนุมานแบบแปรผัน

MAP สามารถใช้เพื่อค้นหาโหมด (หรือโหมดใดโหมดหนึ่ง) ของการแจกแจงภายหลัง แต่ไม่ได้ให้ข้อมูลเชิงลึกอื่นๆ เกี่ยวกับโหมดนี้ ต่อไปเราจะใช้การอนุมานแปรผันที่หลัง Distribtion \(p(\mathbf{W}, \mathbf{Z} \mid \mathbf{X})\) เป็นห้วงใช้การกระจายแปรผัน \(q(\mathbf{W}, \mathbf{Z})\) parametrised โดย \(\boldsymbol{\lambda}\)จุดมุ่งหมายคือการหาพารามิเตอร์แปรผัน \(\boldsymbol{\lambda}\) ที่ลดความแตกต่างระหว่าง KL Q และหลัง, \(\mathrm{KL}(q(\mathbf{W}, \mathbf{Z}) \mid\mid p(\mathbf{W}, \mathbf{Z} \mid \mathbf{X}))\)หรือเท่าที่เพิ่มหลักฐานที่ต่ำกว่าผูกพัน \(\mathbb{E}_{q(\mathbf{W},\mathbf{Z};\boldsymbol{\lambda})}\left[ \log p(\mathbf{W},\mathbf{Z},\mathbf{X}) - \log q(\mathbf{W},\mathbf{Z}; \boldsymbol{\lambda}) \right]\)

qw_mean = tf.Variable(tf.random.normal([data_dim, latent_dim]))

qz_mean = tf.Variable(tf.random.normal([latent_dim, num_datapoints]))

qw_stddv = tfp.util.TransformedVariable(1e-4 * tf.ones([data_dim, latent_dim]),

bijector=tfb.Softplus())

qz_stddv = tfp.util.TransformedVariable(

1e-4 * tf.ones([latent_dim, num_datapoints]),

bijector=tfb.Softplus())

def factored_normal_variational_model():

qw = yield tfd.Normal(loc=qw_mean, scale=qw_stddv, name="qw")

qz = yield tfd.Normal(loc=qz_mean, scale=qz_stddv, name="qz")

surrogate_posterior = tfd.JointDistributionCoroutineAutoBatched(

factored_normal_variational_model)

losses = tfp.vi.fit_surrogate_posterior(

target_log_prob_fn,

surrogate_posterior=surrogate_posterior,

optimizer=tf.optimizers.Adam(learning_rate=0.05),

num_steps=200)

print("Inferred axes:")

print(qw_mean)

print("Standard Deviation:")

print(qw_stddv)

plt.plot(losses)

plt.show()

Inferred axes:

<tf.Variable 'Variable:0' shape=(2, 1) dtype=float32, numpy=

array([[ 2.4168603],

[-1.2236133]], dtype=float32)>

Standard Deviation:

<TransformedVariable: dtype=float32, shape=[2, 1], fn="softplus", numpy=

array([[0.0042499 ],

[0.00598824]], dtype=float32)>

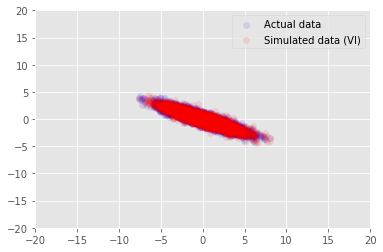

posterior_samples = surrogate_posterior.sample(50)

_, _, x_generated = model.sample(value=(posterior_samples))

# It's a pain to plot all 5000 points for each of our 50 posterior samples, so

# let's subsample to get the gist of the distribution.

x_generated = tf.reshape(tf.transpose(x_generated, [1, 0, 2]), (2, -1))[:, ::47]

plt.scatter(x_train[0, :], x_train[1, :], color='blue', alpha=0.1, label='Actual data')

plt.scatter(x_generated[0, :], x_generated[1, :], color='red', alpha=0.1, label='Simulated data (VI)')

plt.legend()

plt.axis([-20, 20, -20, 20])

plt.show()

รับทราบ

กวดวิชานี้ถูกเขียนเดิมในเอ็ดเวิร์ด 1.0 ( แหล่งที่มา ) เราขอขอบคุณผู้ร่วมเขียนข้อความและแก้ไขเวอร์ชันนั้น

อ้างอิง

[1]: Michael E. Tipping และ Christopher M. Bishop การวิเคราะห์องค์ประกอบหลักความน่าจะเป็น วารสารของสมาคมสถิติ: Series B (วิธีการทางสถิติ), 61 (3): 611-622 1999